|

#1

January 24th, 2014, 04:54 PM

January 24th, 2014, 04:54 PM

| |||

| |||

|

One of my client is engaged in mining of Lignite. To start mining activities, it has to clean surface area and also to dig up Land upto certain depth. The Clay is dumped in nearby area and small quantity is sold without charging duty. Now, whether clearance of Clay without duty amount to what (1) Exempted goods (2) Nil Rate. (According to us there is no CETHN) (3) Goods not manufactured. Whether reversal of Cenvat credit is necessary for common services utilised? Thanks  |

|

#2

December 22nd, 2014, 10:36 AM

| |||

| |||

|

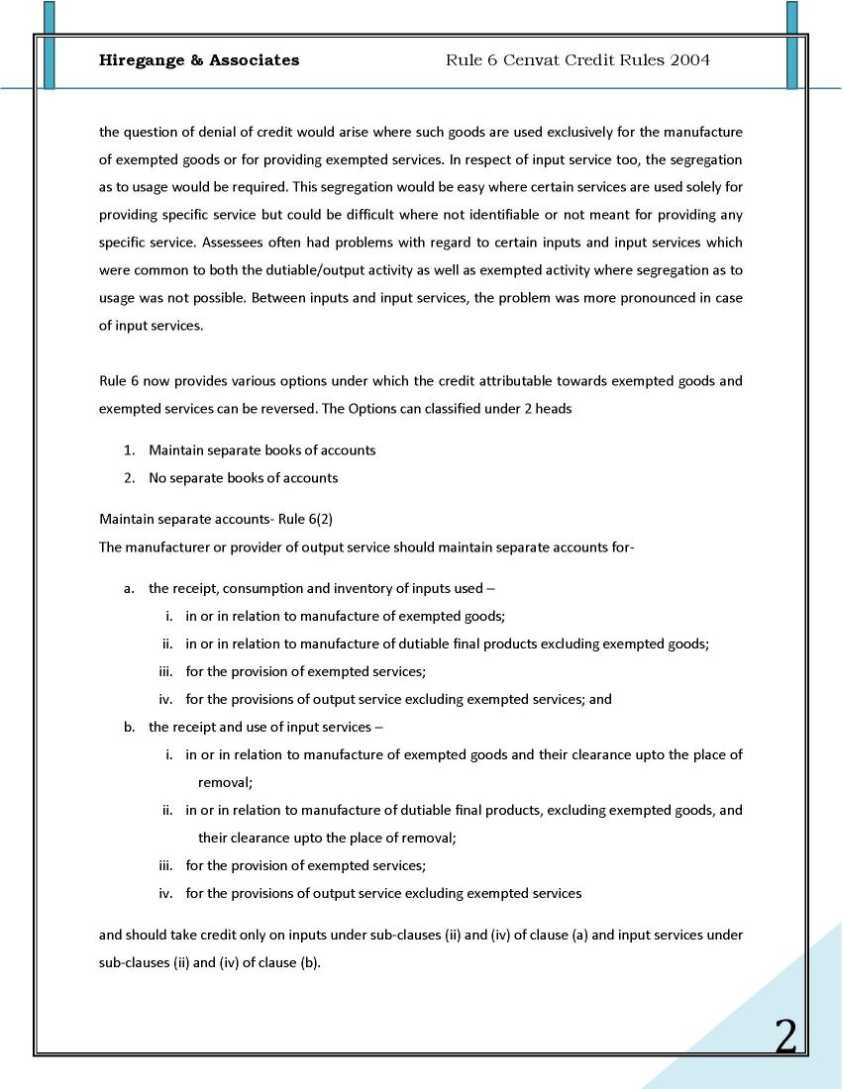

Rule 6 of Cenvat Credit Rules 2004 is important rules from the point of view of a manufacturer of both dutiable and exempted goods and a service provider who provides both output as well as exempted services . Rule 6 now provides various options. The Options can classified under 2 heads 1. Maintain separate books of accounts 2. No separate books of accounts Maintain separate accounts- Rule 6(2) a. the receipt, consumption and inventory of inputs used – i. in or in relation to manufacture of exempted goods; ii. in or in relation to manufacture of dutiable final products excluding exempted goods; iii. for the provision of exempted services; iv. for the provisions of output service excluding exempted services; and b. the receipt and use of input services – i. in or in relation to manufacture of exempted goods and their clearance upto the place of removal; ii. in or in relation to manufacture of dutiable final products, excluding exempted goods, and their clearance upto the place of removal; ii. for the provision of exempted services; iv. for the provisions of output service excluding exempted services     For detailed information, here is the attachment

__________________ Answered By StudyChaCha Member |

|

| |